-

Statutory Audit

We conduct an integrated audit, which combines the financial statement audit,independent and objective assurance on financial information, transactionsand processes.

-

Limited Review

We offer services relating to reviews of historical financial informationby expressing negative assurance on such historical financial information.

-

Agreed Upon Procedures

We engage with organisationsto perform specific procedures and report findings to conform to their needs.

-

Financial Reporting Advisory Services (FRAS)

Our team provides timely advice on the impact of accounting changes to assist businesses in the development of an appropriate implementation roadmap.

-

Business Consulting

Grant Thornton UAE provides organisations with implementable plans that drive sustainable growth strategies to grow and optimise their business performance.

-

Business Risk Services

Organisations need to understand risks thoroughly to be able to manage them better. Grant Thornton UAE helps businesses achieve the best balance between minimising risk exposure, optimising profitability and developing compliance review checklists.

-

Regulatory Advisory Services

Grant Thornton UAE's extensive understanding of the overarching supervisory framework within the region equips our professionals to support financial institutions comply and abide by the set of regulatory mandates throughout the rapidly evolving ecosystem.

-

Financial Advisory

Grant Thornton UAE works with organisations on transactions from start to finish, assisting with strategy, identifying risks, executing deals, and helping to unlock their potential for growth and value creation.

-

Restructuring Advisory

Grant Thornton UAE is committed to realising value for shareholders, in a way that recognises and supports the interests of all stakeholders. Our solutions maximise value, provide clarity and direction, and accelerate recovery and transformation for businesses.

-

Technology Advisory & Cybersecurity

IT and technology are fundamental to drive the performance of businesses. Through leveraging the power of technology, Grant Thornton UAE helps organisations define and identify growth opportunities to achieve value-driven transformation and innovation.

-

Forensics

Fraud and corruption pose a growing challenge worldwide. As the commercial landscape changes, an increasingly regulated environment requires stringent governance and compliance processes. Grant Thornton UAE helps organisations navigate challenges and crisis with a hands-on approach coupled with the use of technology.

-

ESG Services

The Environment, Social and Governance (ESG) agenda has gained significant traction over the years, to become one of the key strategic aspects of any business. It is imperative that all organisations, irrespective of industry sector, engage with their stakeholders and prioritise ESG practices to unlock sustainable growth opportunities.

-

Business Process Solutions

Our team at Grant Thornton offers comprehensive and cost effective outsourced solutions, enabling stakeholders and business owners to focus on their core business goals.

-

Corporate Tax

Our diversified team of corporate tax subject matter experts combines a perfect blend of international experience across several industry sectors, technical expertise, and commercial nuances with a commitment to deliver exceptional value to your business.

-

VAT

The VAT team at Grant Thornton is well versed with the VAT Laws applicable across the region and holds valuable experience and professional accreditation in assisting clients across diverse industries to comply with the VAT obligations.

-

Transfer Pricing

Grant Thornton UAE assists its clients in providing transfer pricing solutions that are implementable and operational, considering the facts and concerns of its clients.

-

International Tax and Tax Due Diligence

Grant Thornton UAE supports multinational groups to optimise their tax structures. We can also assist businesses in analysing existing group transactions and inter-group supplies, as well as advising on potential implications of various taxes to facilitate an efficient Group tax structure.

-

Economic Substance Requirements

Economic Substance rules were introduced in the UAE in 2019, requiring UAE businesses that undertake certain ‘Relevant Activities’ to maintain and demonstrate adequate substance.

-

Customs and International Trade

The team at Grant Thornton is positioned centrally to assist the businesses with global cross-border tax structuring, planning and compliance needs.

-

Excise Tax

We provide Excise Tax related advisory and compliance services to the producer, importer, and the storekeeper of excisable goods

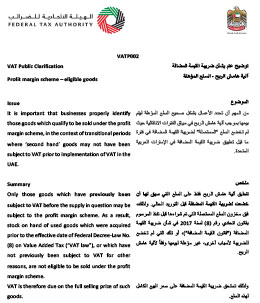

VAT Alert: Profit Margin Scheme Clarification

27 Jun 2018The Federal Tax Authority (FTA) has recently released a clarification on the profit margin scheme for Value Added Tax (VAT) in the UAE.

The profit margin scheme allows a taxable person to calculate VAT on eligible supplies on the basis of the profit margin earned, instead of the original selling price.

The profit margin scheme is applicable on second-hand goods on which VAT has already been levied on the first supply.

Application of the Profit Margin Scheme

The profit margin scheme is applicable only to the supply of certain good. The goods which fall under the profit margin scheme are:

- Second-hand goods − tangible moveable property which is suitable for further use as it is, or after repair

- Antiques − goods which are over 50 years old or more

- Collectors’ items such as stamps, coins and currency

Eligibility Conditions for the Profit Margin Scheme

A taxable person may apply the profit margin scheme to the above eligible goods, subject to fulfilment of the following conditions:

- The goods must be purchased from either an unregistered person, or a taxable person who has applied the profit margin scheme on the same goods previously, or

- Where the input tax on the purchase of such goods was not recovered by a taxable person in accordance with Article 53 of the VAT Executive Regulations.

FTA Clarification

The FTA has clarified its position that the profit margin scheme cannot be used in instances where VAT was not charged on goods, for example if the goods were purchased prior to the implementation of VAT, or if stock is in hand which was also acquired prior to 1 January 2018.