-

Statutory Audit

We conduct an integrated audit, which combines the financial statement audit,independent and objective assurance on financial information, transactionsand processes.

-

Limited Review

We offer services relating to reviews of historical financial informationby expressing negative assurance on such historical financial information.

-

Agreed Upon Procedures

We engage with organisationsto perform specific procedures and report findings to conform to their needs.

-

Financial Reporting Advisory Services (FRAS)

Our team provides timely advice on the impact of accounting changes to assist businesses in the development of an appropriate implementation roadmap.

-

Business Consulting

Grant Thornton UAE provides organisations with implementable plans that drive sustainable growth strategies to grow and optimise their business performance.

-

Business Risk Services

Organisations need to understand risks thoroughly to be able to manage them better. Grant Thornton UAE helps businesses achieve the best balance between minimising risk exposure, optimising profitability and developing compliance review checklists.

-

Regulatory Advisory Services

Grant Thornton UAE's extensive understanding of the overarching supervisory framework within the region equips our professionals to support financial institutions comply and abide by the set of regulatory mandates throughout the rapidly evolving ecosystem.

-

Financial Advisory

Grant Thornton UAE works with organisations on transactions from start to finish, assisting with strategy, identifying risks, executing deals, and helping to unlock their potential for growth and value creation.

-

Restructuring Advisory

Grant Thornton UAE is committed to realising value for shareholders, in a way that recognises and supports the interests of all stakeholders. Our solutions maximise value, provide clarity and direction, and accelerate recovery and transformation for businesses.

-

Technology Advisory & Cybersecurity

IT and technology are fundamental to drive the performance of businesses. Through leveraging the power of technology, Grant Thornton UAE helps organisations define and identify growth opportunities to achieve value-driven transformation and innovation.

-

Forensics

Fraud and corruption pose a growing challenge worldwide. As the commercial landscape changes, an increasingly regulated environment requires stringent governance and compliance processes. Grant Thornton UAE helps organisations navigate challenges and crisis with a hands-on approach coupled with the use of technology.

-

ESG Services

The Environment, Social and Governance (ESG) agenda has gained significant traction over the years, to become one of the key strategic aspects of any business. It is imperative that all organisations, irrespective of industry sector, engage with their stakeholders and prioritise ESG practices to unlock sustainable growth opportunities.

-

Business Process Solutions

Our team at Grant Thornton offers comprehensive and cost effective outsourced solutions, enabling stakeholders and business owners to focus on their core business goals.

-

Corporate Tax

Our diversified team of corporate tax subject matter experts combines a perfect blend of international experience across several industry sectors, technical expertise, and commercial nuances with a commitment to deliver exceptional value to your business.

-

VAT

The VAT team at Grant Thornton is well versed with the VAT Laws applicable across the region and holds valuable experience and professional accreditation in assisting clients across diverse industries to comply with the VAT obligations.

-

Transfer Pricing

Grant Thornton UAE assists its clients in providing transfer pricing solutions that are implementable and operational, considering the facts and concerns of its clients.

-

International Tax and Tax Due Diligence

Grant Thornton UAE supports multinational groups to optimise their tax structures. We can also assist businesses in analysing existing group transactions and inter-group supplies, as well as advising on potential implications of various taxes to facilitate an efficient Group tax structure.

-

Economic Substance Requirements

Economic Substance rules were introduced in the UAE in 2019, requiring UAE businesses that undertake certain ‘Relevant Activities’ to maintain and demonstrate adequate substance.

-

Customs and International Trade

The team at Grant Thornton is positioned centrally to assist the businesses with global cross-border tax structuring, planning and compliance needs.

-

Excise Tax

We provide Excise Tax related advisory and compliance services to the producer, importer, and the storekeeper of excisable goods

The REIT time to invest?

28 Feb 2019The real estate market has been a key driving force in the Middle East and in the wider GCC and has attracted substantial foreign investment into the region over the years.

However, as we all know, much has been said about the demand-supply mismatch in the sector which has caused a general downward pressure in the real estate sector market. Inevitably, a change in investor sentiment creates the demand for innovative ways of diversifying portfolios. The risk-reward spectrum of investors can be better managed if the investment products available in the market can help to create liquidity and diversification to generate capital growth as well as dividend yields.

"REITs provide a liquid investment vehicle to tap into the attractive returns of the Real Estate markets in different geographies. Retail and institutional investors are realising the importance of this growing asset class in the MENA region. Equitativa, manager of Emirates REIT, the largest sharia compliant REIT in the world worth a $1bn, is seizing this opportunity by creating and managing several sector specific REITs, including our $400m Residential REIT, a hospitality REIT, a logistics REIT and other geographically specific REITs, offering investors a wide variety of exposure to diversified real estate assets."

-Racha Alkhawaja, Equitativa Group

Real Estate Investment Trusts (REITs)

REITs, which are a subset of property funds, have been a rapidly growing asset class worldwide and signs of this growth have more recently also been seen in the GCC, enabling access to the region’s vibrant property market to people across the world.

REITs can also help traditional pure play real commercial and residential real estate investors benefit from the growth in specialist areas such as education (e.g. student accommodation), healthcare (e.g. hospitals, clinics) and industrials (e.g. manufacturing facilities).

Global REITs performance

It is interesting to see what level of growth REITs have experienced globally. The chart below depicts the REITs performance across a few selected regions and countries. REITs have been around for a long time now in developed markets such as the US and Europe. They are now having a growing influence in Asia Pacific and the Middle East. The global REIT market capitalisation reached a staggering USD 1.54 trillion as at 31 December 2018, with 37 countries around the world now offering REITs as an investment vehicle, and many more on the cusp of introducing new regulations to join the bandwagon. REITs have been recognized around the world as investor friendly and tax efficient vehicles for investors seeking to leverage returns from the real estate market.

Over the last decade, based on the chart below, FTSE EPRA Nareit Global REITs and the S&P global REITs indices have grown at a CAGR of 17.2% and 12.6% respectively, with the US REITs market experiencing a healthy 17.9% CAGR, Europe with 4.6% and UK 9.8%. Unsurprisingly, the Middle East and Africa REITs index only experienced a modest CAGR of 2.7% reflecting the fact that the market has significant capacity to develop to reach the growth levels experienced in the relatively mature markets. This, however, is also an indication that with the right investment infrastructure in this space, investors can potentially benefit significantly in the years to come.

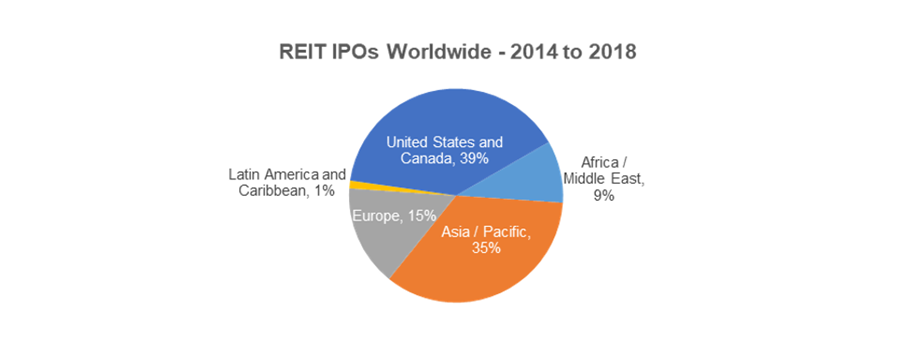

REITs IPOs and their global influence

Over the past five years, there have been 171 IPOs by REITs globally. The United States and Canada have, by far, been the most successful countries for new REITs with a 39% share of total REIT IPOs. In the United States, since their creation in as early as 1960, REITs have grown not just in numbers but also in size, impact and market acceptance and now operate across different sectors in the market.

As at 31 December 2018, public REITs in the US had a market capitalisation of USD 723 billion. Japan, Hong Kong and China made up the largest markets by market capitalisation after the US with values of USD 159 billion, USD 111 billion and USD 95 billion respectively.

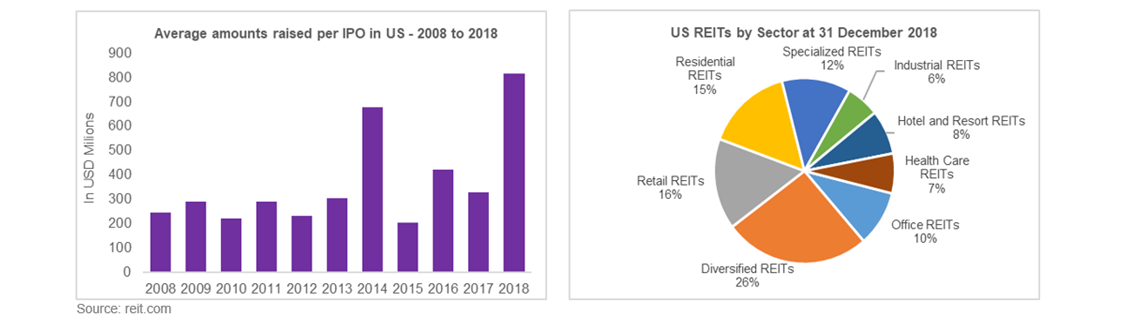

United States

In 2018, US REIT IPOs raised nearly USD 3.3 billion with secondary offerings raising nearly USD 15 billion in light of the strong US markets observed in the first half of 2018. The Retail, Residential and Diversified REITs represent the majority of the REITS in existence in the US market.

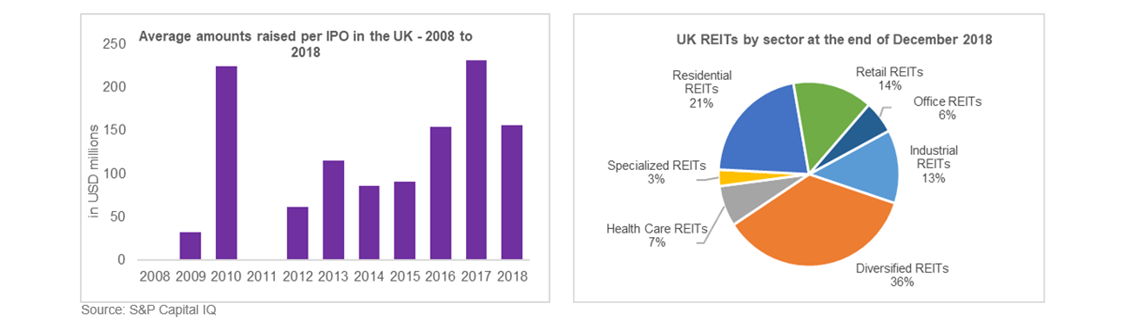

United Kingdom

REITs in the UK gained good traction with 2017 being a record year for the number of REITs floated on the stock exchange. Brexit concerns in 2018 have, however, dampened investor confidence making it a tough year for REIT IPOs. As an example, one of the local REIT indices, the FTSE 350 REIT Index, closed 16% lower at the end of 2018 relative to 2017, reflecting this sentiment. There are currently a total of 52 REITs in the UK with a total market capitalisation of USD 76 billion.

Other markets around the world have also realized the benefits of these investment vehicles, signified by the Asia Pacific region being the second largest market for REIT IPOs. Developed markets such as Japan and Australia are largest by market capitalisation in the region, and other investor friendly regions such as Hong Kong and Singapore have also developed appropriate regulatory regimes to securitize real estate. Rapidly growing nations such as China and India have also moved to develop regulations encouraging REITs, making their future outlook exciting, to say the least.

Looking more regionally, of the total REIT IPOs seen across the world in the last five years, only about 9% of these have been in the Middle East region. In total, the first half of 2018 saw eight public REIT IPOs raising capital of approximately USD 893 million. Of these, the MEFIC REIT Fund IPO, based in the KSA and listed on the Tadawul, was the largest and ended up raising USD 237.5 million.

According to media reports, a number of new REIT IPOs are being planned up including: Manrre REIT by Dubai based Palmon Group which is expected to be listed by 2020; a mixed-use REIT by Dubai Investments subsidiary Al Mal Capital which is set to launch on the Dubai Financial Market; and more imminently, the Shari’ah compliant GII Islamic REIT by Gulf Islamic Investments which is aiming to launch this year and plans to pay out monthly dividends to its investors, unlike the majority of other REITs which tend to pay out dividends quarterly or bi-annually.